Revolut's Puzzle

Revolut is shipping products and launching in new countries at a breakneck pace. Will it grow to be a paradigm shifting company?

Hello everyone and thank you for reading. As a reminder, I write deep dives about fintech - there are so many incredible companies building amazing things and writing helps me to learn more about them. Last week Ron Shevlin profiled me in his column and I got a ton of new subscribers - welcome and hope you’ll enjoy the ride!

Today’s post is about Revolut. I have been thinking about Revolut for some time, but I couldn't really figure it out. It is building on a scale and ambition that I haven’t seen others attempt - a combo of Chime, Robinhood, Marcus, and Step for retail customers, and Mercury, Brex, Stripe for businesses, all in 35 countries and counting. So I set out to unpack it because I think it is one of the most interesting companies right now.

On the weekend I stumbled upon some old medium posts from Alex Danco about technology and innovation (here and here) - he is excellent and I recommend you read the entire series. Some things clicked. I listened to a couple of interviews of founder Nik Storonsky, who I think needs a separate profile piece (strong personality he built Revolut on his own image, still owns a third of the company and has a skin in the game). So I am putting together a Revolut thesis. I would really love your thoughts, so feel free to comment or DM me!

From scarcity to abundance

Alex writes that revenues are made at a point of friction where resources are scarce - money, time, access, convenience are exchanged for a premium. Incumbents guard the scarce resource as much as they can because that’s how they make money. New technologies remove that friction by giving a new access to the scarce resource and that’s how incumbents get disrupted. The walls they built around their treasures disappear. All major tech companies of today have abstracted away a previously scarce resource - Microsoft and PCs, Google and indexed internet, Amazon and convenience, Uber and transportation, WeChat and P2P interactions - effectively replacing companies and business models that stood before them.

Naturally products that make turn scarce resource into abundant supply have an instantaneous product market fit - customer numbers swell and VCs pour money. Just think about an array of transportation, food delivery, and closer to home - fintech companies that were funded at the same time along the same verticals. However, often these startups get stuck in the old modes of business construction - having unleashed abundance, they struggle to make money. High expectations built on top of a great product market fit crumble, and unfortunately many startups fail.

But then someone somewhere discovers a new scarce resource, which then leads to a paradigm shift: Microsoft and distribution, Google and advertising, Amazon and customer loyalty, Uber and drivers, WeChat and identity. New business models replaced the old ones - e.g. Google is free to use because friction is elsewhere, Amazon can pressure prices down because customers are on Prime, etc.

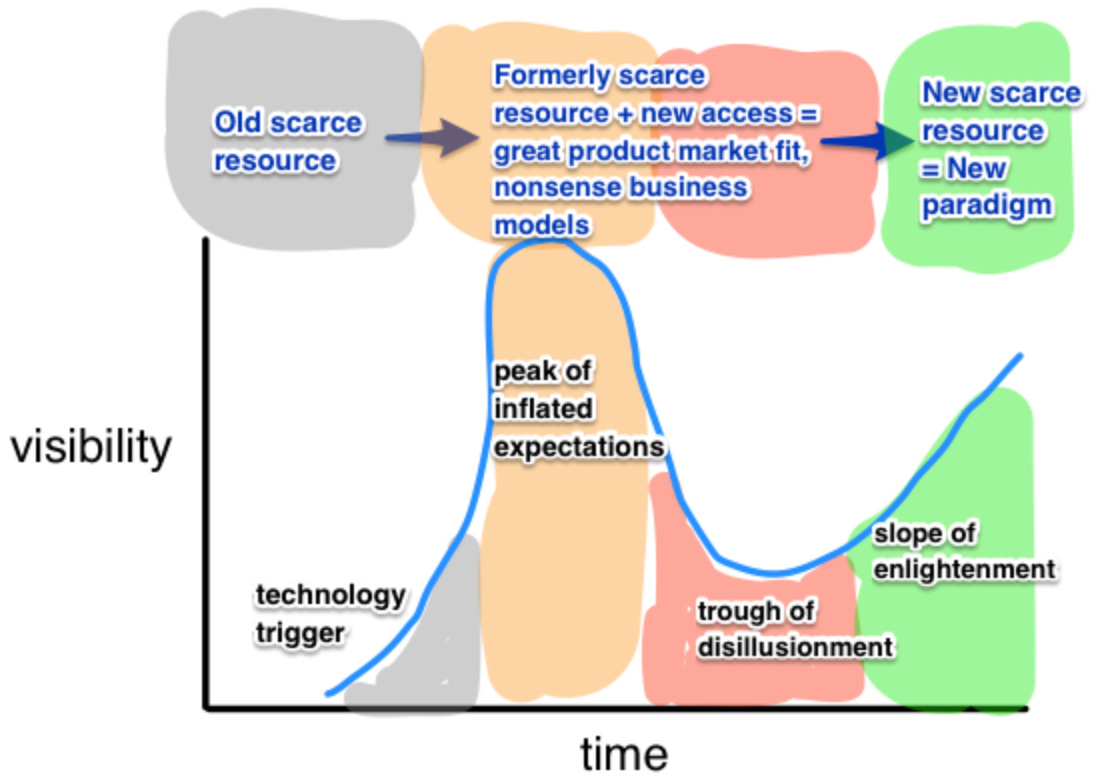

Alex uses the Gartner hype curve to demonstrate the point.

This model almost perfectly applies to a fintech space which is one of the most exciting new industries of the last decade. CashApp started by abstracting away scarcity of P2P payments. Monzo started by eliminating complexity of everyday banking. Revolut started by giving access to cheap international transactions.

However, unfortunately a lot of fintech companies are still stuck in the trough of disillusionment - i.e. an area where formerly scarce resources are released, but none created anew. Combining new access with a previously scarce resource doesn’t result in any good business model - it’s difficult to monetise. Very few fintech companies have identified a new scarcity necessary for exiting the dip. Square has found one with CashApp, and is moving towards a new one - connecting buyers and sellers in the ecosystem. Stripe abstracted away online payments, but realised entrepreneurs need back office support and treasury management. Shopify abstracted away the complexity of opening online stores, but unleashed a direct-to-consumer revolution. Coinbase gave access to a totally new scarce resource.

It is no coincidence that paradigm-shifters are all high speed/velocity1 companies because as they build more things they inch closer towards a new paradigm (that is if they listen to the signal vs dogmatically following their setup vision). This brings me to Revolut - it is probably one of the most high product output companies in fintech right now.

I have to admit though, I couldn’t really understand their product strategy. Shipping products across different verticals and use cases, at the same time as launching in new countries, all without clear focus and differentiation from competition, to me looked like they were randomly building what’s hot - e.g. crypto, trading, business expense management, online payments acquiring, US market, Chinese market.

But applying a scarcity-abundance-scarcity framework helped me to make some sense. I think Revolut is making bets on two new paradigms:

Global super hub: one financial account for anywhere in the world

Merchant banking super hub: businesses need to consolidate all finance flows into one place - sales, suppliers, payroll, business expenses, treasury

Are these hypotheses going to help Revolut to become a paradigm shifting company? It’s really hard to predict, although I am more optimistic about (2) than (1). But because Revolut is so fast2, relentless and so ambitious, they probably have a better chance at climbing up to the slope of enlightenment.

Global super hub paradigm

Founder Nik Storonsky said the idea for Revolut emerged when he saw how much banks were charging on overseas card usage. He spent six months learning about how bank payments work. In “your margin is my opportunity” fashion, Revolut set out to disrupt the business for incumbent banks in that specific niche. The company was founded in 2015.

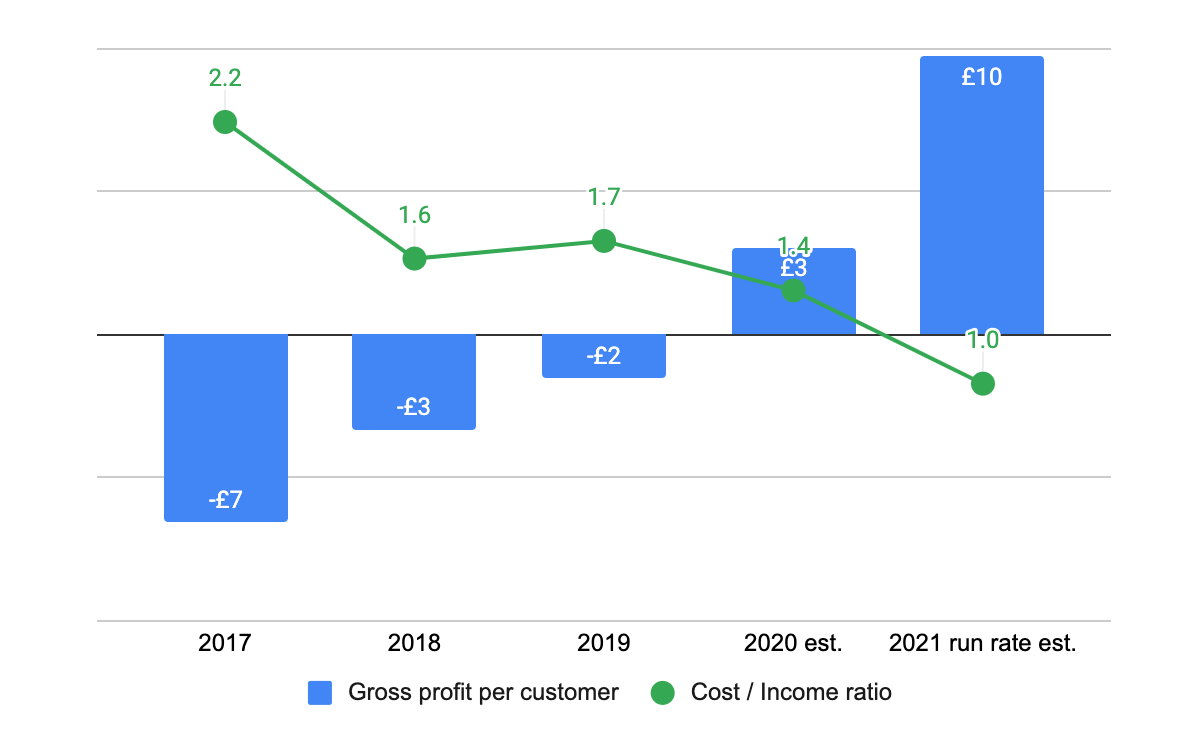

Revolut gave access to a previously scarce resource but hasn’t replaced it with a new one. Although product market fit was established (Revolut grew faster than other neobanks), the business economics didn’t work. International card spending is lucrative, but as any “flow” business it relies on scale (it is usually harder to increase customer’s propensity to spend). However, every new customer cost more money than the revenues they made. Back in 2017 on average a customer was making £12 per year, but cost £19 in direct expenses such as onboarding, customer support, fees to share. Revolut needed to find the edge.

So the product shipping conveyor started soon after and really kicked off post 2018 with the aim of finding a profit driving lever. Departing the FX top up card vision, Revolut effectively built a destination point for all financial needs, and started calling itself a super app. This has culminated in the recent app relaunch that looks very familiar to eastern super apps.

Today’s Revolut mission is grand:

We are building the world’s first truly global financial super app. In 2015, Revolut launched in the UK offering money transfer and exchange. Today, our customers around the world use dozens of Revolut’s innovative products to make more than 100 million transactions a month.

How is that working out? Things have improved, so much so that Storonsky says they are now profitable on a monthly basis (more on that later).

But who is the customer? Original FX offer meant that Revolut was acquiring customers who were looking for cheaper FX cards - those who travel abroad to work, holiday or study. So Revolut decided to follow these customers and offer them more than a FX card. Its strategy became dependent on expansion.

Revolut has expanded beyond its home market of the UK into 35+ countries. The global expansion has had mixed success - in Ireland for example Revolut is ubiquitous, whereas it had to abandon Russia and Canada for different reasons. But that scale allowed them to practically build up a new country playbook - Storonsky said they allocate $20-25 million per country and expect 2 years before payback. Incidentally, the newest expansion is going to be in India where they hired a new CEO and budgeted to invest $25 million.

As a sign of its ambition, Revolut is expanding to the US and China - the hardest markets to compete in right now (Russian market is on par). Revolut applied for a banking charter in the US, and recently Storonsky said they have invested $100 million, and plan to spend $20-30 million this year on advertising. Revolut has 260k customers on beta, compared to just 100k of N26 that has probably spent tens of millions on advertising. I think Revolut’s US customers look promising, and that’s what the newest fundraise thesis is about - to boost up US expansion. As an indication of potential investments needed, Square has spent about ~$1 billion since it was founded (proxy here is retained earnings). However, as Revolut’s focus will be on expats and travelling people rather than the entire population, its customer numbers wouldn’t ever reach 35 million of CashApp’s, but they can profitably serve couple of million.

China plans are very fresh - it is impossible to break the grip of WeChat and Alipay but the likely plan there is the same: serve those who travel, study and work abroad.

Storonsky said he looks up to WeChat and Alipay, and a lot of what Revolut is doing is partly inspired by them. For example, they showed that the more products there are on the app, the lower are acquisition costs relative to the value these customers bring. Customers need to be brought in only once to use a growing variety of products which increases their LTV.

So Revolut is building one of the most rich banking offers, which is also amplified by the pricing - Revolut was one of the first neobanks to introduce subscription bundles. By some accounts in 2019 close to half3 of daily active customers were on paid plans. Recently they introduced Plus at £2.99 per month, which probably boosted subs numbers higher.

Bundled pricing serves well for a high velocity product roadmap - by adding more products, Revolut increases the value of a bundle to customers, boosting their loyalty and increasing the friction of switching (scarcity). Customers come for one product, stay for the bundle. That increases usage and retention, as well as LTV, allowing for a better LTV/CAC ratio.

There is no denying that decisions are made fast at Revolut, and are followed through. Storonsky allocates capital based on what is more promising. There is a beauty in that. But Revolut’s global financial super hub vision is still a bit disjointed, because it is very broad. Where CashApp builds only adjacent products to boost its network, Revolut crams all financial aspects into one app. But today it is very easy to maintain financial life across several products - all specific and tailored solutions are an app download away (lending, insurance, pensions, investments, P2P), so switching costs are really low. Not to mention the challenges of local regulation and product adjustments needed to compete in many countries. There are definitely “underserved” international living people who are the target for Revolut, but the super hub vision might have a better application in business banking where switching costs are much higher.

Merchant banking super hub paradigm

Revolut launched business banking accounts in 2017, but relatively recently started investing heavily in it. Storonsky now talks about an ecosystem similar to what Square is doing with the Seller side and CashApp.

Some of the new builds include online payment acquiring and CFO office suite products such as expense management, corporate cards, and soon to be launched payroll. This effectively combines business banking with products like Stripe/Adyen and Brex/Ramp.

I do see an appeal of a product like that for a business banking customer. There are underserved users in that segment - why keep merchant and bank accounts separate when combining them would make life easier. Both Square and Stripe, having started from payments now offer banking: Square opened a SME bank, and Stripe has partnered with banks.

Revolut competes with them on pricing but payment companies started from a narrow focus and incremental thinking which result in a superior product. This thread about Postmates increasing revenue by $70 million since moving to Stripe is illuminating - Paul Graham asks why companies make more money with Stripe, and Patrick replies:

It is hard to imagine anyone displacing Stripe right now. The grunt work is hard and divests engineering resources from other opportunities, especially if payments is not the main focus of the company. Would it pay off for Revolut? Well, Revolut’s business banking performance is looking good. Storonsky said revenues tripled during the pandemic, and sure, a lot of it is on the back of a crypto wave. But the overlooked element and what Revolut is not generally know for is their business banking foray. In September 2020 they had 500k customers - Storonsky said customers doubled during the pandemic. For reference Starling Bank which saw its UK business banking customers soar on the back of giving out covid relief loans has about 300k business customers today.

Business banking is much more lucrative, on a per customer basis at least 10x more so, and it is a hedge against volatile consumer trends. By adding more products to the suite that compete on performance, business banking can help Revolut carve out a niche serving those entrepreneurs who trade globally in different currencies. That’s why they won’t be competing against companies like with Square or Mercury who focus on local service. Here, similar to retail vision, Revolut is building for internationals, but unlike in retail, business has more money and less competition. This vision to me looks more promising.

Are profits sustainable?

Storonsky said Revolut had about 20 million customers as of April. The company raised close to $1 billion from a host of investors including Index Ventures, DST, Ribbit Capital. Revolut is currently raising at a $10 billion valuation.

Revolut was incurring large losses until recently - last year it made a £106 million loss (almost £9 million per month), up from £33 million in 2018. Not only Revolut had low ARPU vs other fintechs and banks, its margin and cost structure wasn’t that appealing also. Added to that costs of expansion, and losses were going up.

Pandemic has been a major boost, and Revolut repositioned itself as a crypto and stock trading destination, as well as a business bank. In addition, Storonsky said they have optimised business costs. As a result, Revolut turned profitable on a monthly level. Back in 2017, for every £1 earned, Revolut was losing over £2 of VC money. Today they are earning more than spending, so the ratio has flipped.

Revolut made £162 million of revenues for the full year of 2019. Two thirds of that was from interchange, and a quarter from subscriptions, with the rest being commissions from trading and other activities. During the early pandemic, revenue fell off 40%, but since then it tripled and gross profit increased 10x. This means the product stack has changed significantly towards the high margin commission business.

In 2019 Revolut traded about £130 million in crypto (£56 million bought, and £64 million sold on behalf of customers), those volumes have surely increased by a multiple in 2020-21. For reference, Coinbase volumes increased from $80 billion to almost $200 billion from 2019 to 2020. Business banking customers doubled, driving substantially higher unit economics. Margins have probably increased from ~20% to ~70% range. So even though the revenue per user is at a lower end vs other banks and fintechs, margins of 70% applied to a larger scale resulted in a nice payback.

Travel is gradually returning, crypto is here to stay, and Revolut’s larger focus on more accretive business banking would pretty much guarantee gross margin expansion.

Revolut has built up an amazing execution muscle and is a product led company, turned profitable. The scale and breadth of Revolut’s ambition as well as its execution cadence is apparent, but it seems like they are fighting many battles simultaneously. Lack of focus concerns me - I believe that a company with a broad based mandate will always be vulnerable to a challenge from a sharply focused startup.

However, that’s why fintech is so exciting. Fintech companies are pushing boundaries, rethinking game rules, and uncover trapped demand that customers didn’t even know they had. Predicting paradigm shifts is hard and a lot of things current tech giants pivoted to sounded illogical at a time. Revolut is so bold, I am rooting them to succeed.

One non obvious benefit of product velocity was articulated by John Collison of Stripe on Invest Like The Best podcast. He said that employees find it much more enjoyable to work at a company that’s moving fast. This is also true for hiring - smart people want to work on interesting things.

This essay by Frank Slootman (legendary tech CEO currently at Snowflake) that he wrote when his previous company ServiceNow IPO’d brilliantly articulates the value of speed and trade offs that are made. He also writes about importance of focus, which is what Revolut is lacking

They had 250k daily active users sometime in 2018, and then reported growing them by 230%, to 830k. Subscription revenue in 2019 was £39m, implying average cost of £8 per month, translated to 390k subs. 390k/830k=47%