Understanding Klarna

Plus: CashApp average customer behaviour and Kaspi.kz financial results

Hello and thanks for reading! Today I wrote about three companies.

Klarna. All major BNPLs are moving in with offering a consumer banking product to build direct financial relationships with shoppers. Klarna had a head start - it has been a consumer bank in Sweden since 2017 and is now launching it in Germany.

CashApp. When CashApp repositions itself as the main bank account for customers, its revenues will probably fall (before growing back up).

Kaspi.kz. A fintech bank from Kazakhstan is on fire, operating out of the tiny market of Kazakhstan (check out this video of my home country), it has generated an incredible 70% RoE last year. It is one of the best examples of closed loop ecosystems between consumers and merchants.

Caveat: this is not an investment advice, etc., etc., etc.

Understanding Klarna

Covid pandemic has compressed years of online commerce progress into just several months.

Some of the biggest winners of the shift are Buy Now Pay Later (BNPL) companies - AfterPay, Affirm and Klarna all benefited from rising valuations and funding. But as the space is hotting up, all big finance players are entering the field from PayPal to Goldman Sachs. Large companies like IKEA and British Airways are integrating their own BNPL options as well. A slew of smaller and niche players are being funded too.

BNPLs are so very popular because they appeal to both consumers and merchants:

Consumers: With BNPL positioning not as a credit, but as an easy way to spread the cost of purchase, its popularity for consumers has skyrocketed.

Merchants: BNPLs deliver better conversion rates, order size and frequency of purchases. Klarna did a research on Shopify merchants and saw that 44% of customers wouldn’t convert if they didn’t have a pay later option available. Affirm claims to increase the order size up to 85%.

As an extension, BNPLs make most of their revenue from merchants, and until very recently they didn’t have financial interaction with shoppers outside of the shopping experience. That is changing as they pursue a two-sided platform path.

BNPL as a platforms

Merchants embed BNPL as checkout option on the page or app, but the battle for checkout is being fought on all fronts - from payment gateways, to digital and crypto wallets (this write up of the said battle is great). As checkout options proliferate, the payback from real estate is diminishing.

One way to hack the distribution is to partner with aggregators, e.g. Shopify+Affirm, or Stripe+AfterPay. This position, however, doesn’t build up any sustainable protection as aggregators could switch or add more providers, or even build their own versions of BNPL. As a result, all major BNPL companies are adding consumer financial products to maintain relationships with shoppers outside of the shopping cycle and personalise offers to drive effective purchases. Here are some of the recent news:

Executed well, this would transform BNPLs from a merchant checkout option to a two-sided platform with demand and supply.

If in addition to better conversion, order size and repeat purchases, BNPLs could drive the purchase intent and large traffic, they would be immensely more valuable to merchants.

Among the three largest companies, Klarna has advanced the most in its consumer product - Klarna has been a regulated bank in the EU since 2017 and used customer deposits in Sweden to fund its ‘pay later’ products. It is now launching a bank in Germany, partly to solve a funding gap, but also to scale its customer offer.

Klarna Bank

I wrote before that being a bank is costly. One of the biggest indirect costs is a capital requirement1. But on the upside, being a bank allows Klarna to control the entire value chain and keep all proceeds, and gives it freedom in its product development. Being a bank hasn’t precluded it from geo-scaling either.

But as a bank Klarna hasn’t set the lending flywheel yet.

Lending performance is weak (no flywheel yet)

Unlike other BNPL companies Klarna controls its entire supply chain from origination to repayment. Both ‘pay later’ products and interest bearing loans are part of the loan portfolio for Klarna and are in majority funded by deposits from customers. As of Dec-20 ‘pay later’ products comprised about 60%2 of its total loan book. The rest is for longer term interest bearing loans at APR of ~20%. That’s why on average the entire loan book yields about 9%.

Naturally, “pay later” products have high velocity - average portfolio duration was just 40 days, so Klarna could recycle the same funding as often as once a month, whilst keeping the book balances stable. It is those balances that Klarna needs to hold capital against.

Klarna’s capital requirement as of Dec-20 was SEK 4.9 billion, or roughly $580 million vs. ~$750 million of total equity it had before the $1 billion fundraise. Majority of that requirement of about ~$400 million is from credit operations or loans to customers, which on a per $1 loan basis works out at about ~8p.3

Now circling back to the average yield of 9%, almost all of the interest income the loan book generated within a year went into supporting its capital position. But add to that the cost of funding and credit losses, and Klarna’s loan portfolio performance is not actually very good.

Assuming Klarna’s lending book has a direct capital claim of $400 million, the business will be capital accretive when it has earned more than that. But Klarna’s lending business in 2020 earned only $16 million, or 25x less than the capital requirement.

To accelerate the payback on lending book, it needs to grow gross yields by giving out more interest bearing loans and do better with credit decisioning as credit losses are high. Should it increase gross yield to 15% (from 9%) and reduce credit losses to 5% (from 8%), the payback will be shortened to 1 year (still less than the average duration of the loan, but the impact of change is non-linear).

But commission business covers all of it and then some

Capital requirement is a cost to Klarna of keeping all of its revenue, including commission income. As long as the capital requirement is covered by total proceeds, it doesn’t matter how it is funded. Case in point - Klarna’s net commission revenue in 2020 covers its entire capital requirement with a 40% surplus.

Looking through this angle, the lending business was actually a net positive, adding $16 million of net yield. But the question is could Klarna instead direct the funding to its commission business, given it is so much more effective? That’s definitely what’s happening - the share of interest bearing balance went down from about 50% to 40% within a year.

Capital allocation problem

So Klarna has two businesses and they compete for the funding:

Interest bearing business needs long funding, is based on writing long term loans and accruing interest of 20%.

Commission business on the contrary has high velocity and can’t work effectively if the funding is held up in longer term loans. It recycles the same $1 up to 12 times a year, earning commission from merchants every time. Average take per GMV last year was about 2%, so 2%x12=24%. Today it is commission income that makes Klarna bank sustainable.

But the same commission business is under pressure from increasing competition from other BNPLs. Scaling a banking product is designed to protect and grow commission business via cultivating customer demand. But it can’t be sufficiently realised without growing the lending business to entice and bring more customers on the banking product.

This is a really interesting capital allocation problem. Luckily for Klarna, it raised a ton of money recently, has a massive customer base, and a capital accretive business. These things usually solve many problems.

CashApp customer behaviour

Square released the latest financial results. One thing stood out to me - the amount of money CashApp makes from instant deposits:

Assuming the numbers above, last quarter CashApp made $170 million from instant deposits. This translates to $11 billion of volumes at 1.5% fee, or ~$100 per customer per month. That sounds like a lot for an average customer.

So I got curious and decided to look into average CashApp’s customer behaviour (caveat - averages are misleading)4.

On a very high level wallet cash flow would include:

cash inflow (direct deposits of salary or tax credits, and top-up from debit card)

spending (shopping, groceries, etc.)

investing (stocks and bitcoin - these could be both inflows and outflows and for this exercise I assume that people are buying rather than selling)

withdrawal (ATM and transfers out, including the above instant deposits)

p2p transfers could wildly differ from customer to customer, but at a system level they cancel each other out (this is where average is also misleading)

Looking at Q3 and Q4 balance sheets, the average balance per customer was between $53 and $56, so I assume that each month an average customer starts with $55 and ends with $55. Here is the waterfall of monthly moves on an average CashApp wallet:

Looking at the waterfall, what jumps out to me is that the average customer doesn’t use CashApp fundamentally as a bank and that there is no unifying behaviour. It shows that there are distinct group of customers who use the product very differently:

Power users (a subset of Cash Card adopters that put salary in, spend and save)

Small and active minority of bitcoin/stock traders (average volume per bitcoin customer was about $580 last quarter, again buy+sell)

P2P/Wallet users who transfer money in and out of debit cards

There are obviously intersections of Venn diagram - for example, the fact that instant deposits revenue is the largest probably means that it appeals to a higher proportion of customers.

CashApp is profitable because it charges a fee on cash flows, so for the moment it doesn’t matter that balances are not growing. All the products are designed to encourage people to move money more frequently - bitcoin, stocks, boosts.

But as CashApp re-positions as the main bank account (now depositing salary unlocks some extra boosts), its highest revenue source will decline - people won’t need to “instant deposit” that much if they use the account as the main one (this is of course based on the assumption that people instant deposit mainly to themselves). Subsequently, balances per customer will start building up which then opens a way for lending.

So at a simplified high level, as CashApp repositions itself, revenues will first decline caused by reduced volumes of instant deposit transfers, before they increase on the back of interest income. Would that work? Would love to see the capital allocation analysis the team is running now (in addition to Klarna’s).

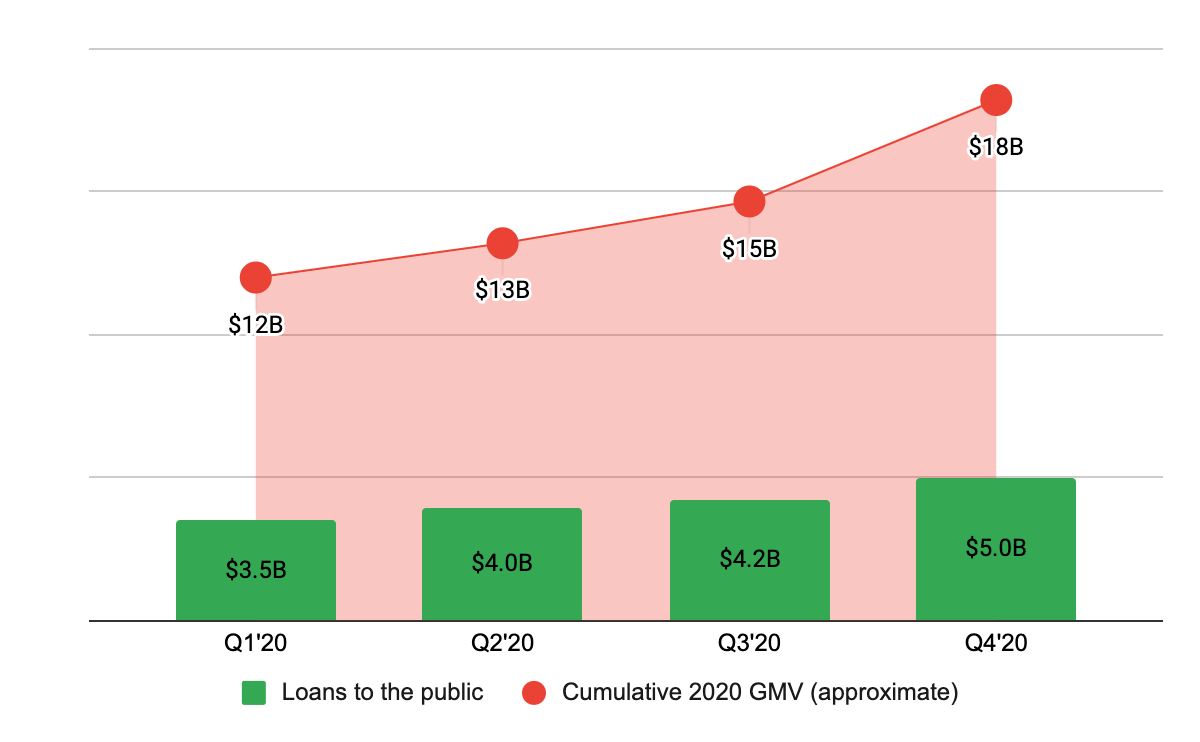

Kaspi financial results are out

Kazakhstani fintech Kaspi.kz published their 2020 financial results (I wrote about them here). Net income grew 43% whilst retaining a net profit margin at 40%+ (Q4’20 net margin was 49%!).

Two key things stood out:

the business is shifting away from lending with its share of net income down from 72% to 54%. Most of the lending business is now BNPL products.

increased focus on merchants with a broad range of new services.

Practically, investments in merchants solutions resulted in a share of Kaspi’s in-store acquiring growing from 4% to 38% within a year.

Kaspi has an incredibly strong consumer offer and having invested heavily in merchant offers, it is closing in on the loop of its ecosystem. This allowed it to generate some extreme profits with an RoE of 70% (Tinkoff had a 50%). So much so that it distributes half of its net income in dividends, to the tune of $320 million.

I am really keen to see Kaspi start its geo expansion. But it would be hard to compete with a 70% return rate for any new growth and investment plans. Are they ready to get a hit to those RoEs?

Capital requirement is not a cost to a business the same way salaries or marketing are. Banks need to reserve a portion of their equity to protect it in case of some collapse. That means that banks can’t use up all of their equity or fundraising to burn through for growth the same way any other startups could. In fact, before the most recent $1 billion fundraise, Klarna’s capital requirement was about 3/4 of its entire equity, so it could have only used 1/4 of its equity to fund the growth.

Klarna doesn’t report the split, but high level triangulation between interest income, known product APR and total lending balances show it was ~60% at Dec-20.

Derivation from its capital filling - capital requirement as % of total exposure is about 12%. Lending exposure is 75% of a lending book. 75%x12%=~8%

There’s a Russian joke that goes “One person is cooling in the morgue, the other is running a high fever. The average temperature in the hospital is 36.6 C though”