Tinkoff and Russia's Ecosystems

In Russia, everyone is building ecosystems - Tinkoff, Yandex, Sber, Mail.ru and many more. But Tinkoff is a great bank and perhaps it should stay as such.

Tinkoff started from lending and with 50% RoE it is the largest profitable neo-bank. It wants to become a lifestyle partner to customers by building ecosystem of financial and non-financial products. I don’t think it is currently working out and I believe Tinkoff should double down on what it’s good at - being a great bank.

I was inspired by CEO Oliver Hughes who has been on several podcasts lately. I also read a book by Oleg Tinkov, a founder of Tinkoff Bank called “Revolution. How to build the largest online bank in the world”1, a fascinating account of ups and downs of Tinkoff Bank from 2006 to 2018. It is unfortunately in Russian, as are many sources here (sorry!)

Hope you’ll enjoy the post, and by the way, welcome to many new subscribers - my last deep dive on CashApp has been the most popular to date. Thanks to Simon Taylor and Nik Milanovic for featuring it.

Oleg Tinkov is a hustler, the type of entrepreneur who would have been successful at any time. During Soviet period he was active in black markets - buying and selling things like jeans, sneakers, and even hockey sticks. From then on he founded and sold a succession of ventures including white goods stores chain, ready made meal company, brewery and chain of restaurants. He sold Tinkoff Beer to AB InBev in 2005 for ~$200 million. A semi-professional cycler, he owned a pro cycling team Tinkoff. Under his other business La Dacha he rents out his luxurious properties around the world, and recently launched a world first ice-breaker yacht that could be rented from 740k euro per week (!).

Strong personality, Tinkov has many critics because of his blunt and cocky style. He thrives in confrontation and is extremely self-confident (unlike in the West, naming a business after oneself is still very rare in Russia). Forbes list billionaire, he is a rare self-made businessman who is not politically connected (though he supports Putin which is probably a minimum required effort to run a large business in the country).

His biggest business is Tinkoff Bank with the current market capitalisation at over $8 billion. Started as a monoline credit cards business, it is now transforming to a lifestyle Super App.

Tinkoff - origins

In 2006, using proceeds from the brewery sale he invested $60 million and hired a strong management team to launch what is now called Tinkoff Bank (Tinkov was chair of the board, Oliver Hughes was CEO). Originally modelled after US Capital One, it was a credit card company that was wholesale funded by institutional investors. Oleg Tinkov quoted Nigel Morris, co-founder of Capital One, who told him: “credit business is like playing with fire: come too close and you will burn, too far - and you will freeze”. Tinkoff Bank mastered the proximity and very quickly became profitable.

At the time, Russia’s retail banking infrastructure was very well developed2. In Soviet times people were encouraged to deposit savings at Sberkassa (State Savings Bank which is now known as Sberbank or Sber). Almost everyone would have a savings account, even children, so people had an embedded experience of banking. After Soviet period many banks started working with companies to launch salary projects - bank accounts and debit cards were issued en masse to employees.

By the early 2000s debit cards and ATM machines were well penetrated. In addition, Russia’s economy was booming with high oil prices and optimism around young President Putin. People started spending more and looking out for credit. A big wave was coming.

Tinkov writes that to ride that wave he needed a lot of wholesale funding, which he could only get if he had a credible business partner, such as Goldman Sachs who in 2007 bought a small stake. After IPO in 2013 Goldman Sachs cashed out 15x on the initial $15 million investment. It is not a coincidence that Goldman Sachs has also invested in Kaspi from Kazakhstan, and reaped handsome IPO rewards last year - they know how to make money in post Soviet countries.

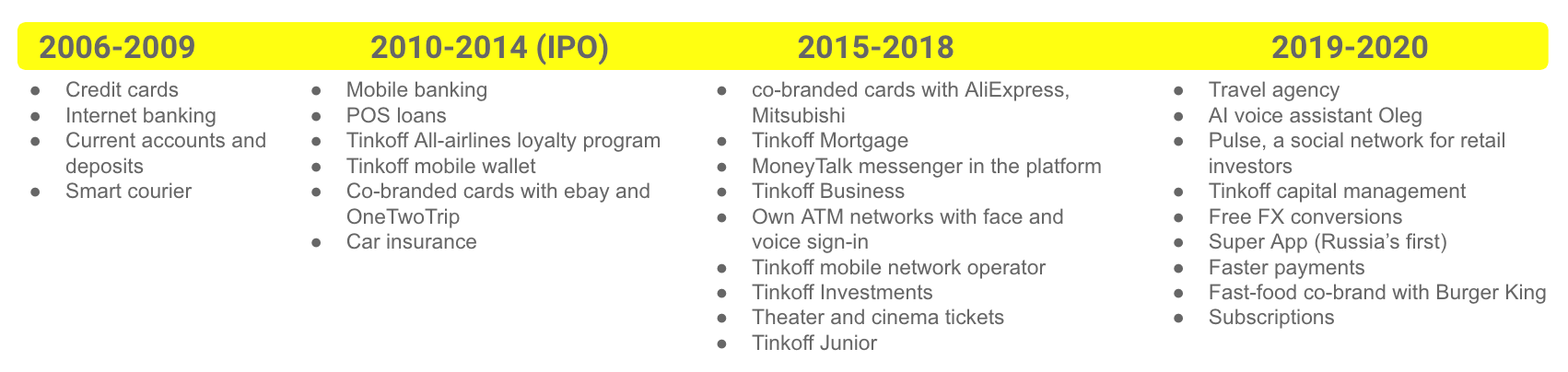

For Tinkoff Bank all was going great until the global financial crisis of 2008 dried up institutional funding. To solve the imminent funding problem, Tinkov somewhat reluctantly was persuaded by his team to depart from his favourite model of monoline credit cards business. That year Tinkoff Bank launched debit cards and current accounts, effectively becoming a comprehensive everyday bank. Tinkoff was branchless from the start, so it effectively became a pioneer of neo-banks before the term was invented.

Tinkoff calls itself a tech company, and its velocity of innovation is a testament to that.

Tinkoff today

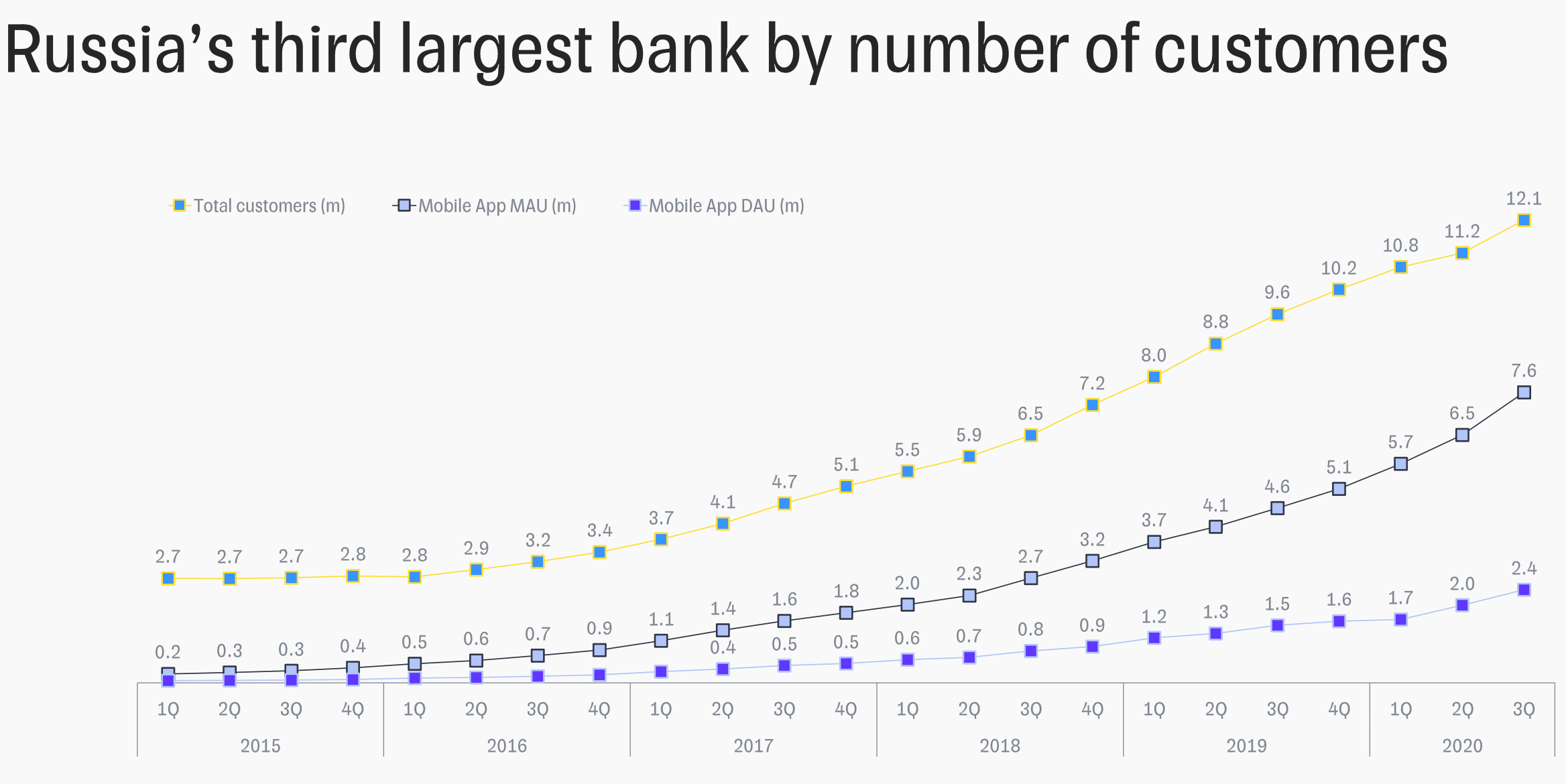

Tinkoff grew quickly, and today has 12 million customers, which is >10% of market share. It is the 3rd largest bank and plans to become number two by growing to 20 million customers in the next three years. Crucially, unlike western neo-banks, Tinkoff provides a full banking experience so it is more likely customers use it fully and not as a spending card.

The growth spurt started off from mid 2017 is a result of extensive product innovation and addition of adjacent services that had customer value, e.g. Investments, co-brand partnerships, etc. These new products provided more cross sell opportunities making Tinkoff extremely profitable - it has a market winning RoE of close to 50% and net income margin of 20%. Last quarter it made ~$160 million in net profit (+30% yoy) and is on target to reach $1 billion in annual net profits.

Adjacent financial services have diluted the share of credit revenues - last quarter 40% of total revenue came from non-lending financial products.

On average customers make over $200 in annualised revenues. But in Russia competition for customers is intensifying and there is one competitor that grows stronger and stronger.

Sberbank, the giant

Sberbank, the largest and oldest bank in Russia (descending from the Imperial times), is an absolute mammoth with 96 million customers that employs 280,000 people. With 13k branches in 85 regions of Russia, Sberbank’s coverage is equivalent to postal services. Russia is of course a large country and in small towns and villages Sberbank might be the only banking service. However, it is still telling that the 2nd largest VTB bank had less than 14 million customers last year.

According to a Deloitte research, a whopping 87% of surveyed Sberbank customers were monthly active with average annualised revenue per user, a double of Tinkoff’s (Sberbank does mortgages and corporate banking). So it is not only the largest, it is also extremely profitable with RoE close to 20% (remember - it is after costs for 280k employees and 13k branches). Last quarter it earned ~$3.5 billion of net profit, more than the global HSBC.

In 2007 Herman Gref was appointed as the head of Sberbank. A young and progressive ex-finance minister he came with a vision. Since then Sberbank went through an unprecedented digital transformation of any large bank in the world. Gref wants to transform Sber into a tech company and sees Google and Alibaba as competitors.

He went on a shopping spree buying 11 companies including Rambler (was one of the largest search and news aggregators), partnering with Mail.ru Group (owner of Russian social network vk.com), and with Yandex (Russian version of Google) to offer Sberbank customers a wide array of non-financial products. Sberbank has invested close to $1 billion into its non-financial ecosystem - no one in Russia has that kind of money for product development.

Gref’s vision of the Sberbank ecosystem is “surrounding customers with convenient digital services for every occasion”, including food delivery, shopping, video and music streaming, healthcare, education, ride hailing, mobile operations, logistics and courier services, and job search. Of course all financial products are included too.

Recently Sber started reporting ecosystem metrics, and have earned close to $0.5 billion last year and planning to double that. More than 60 million customers are active users of mobile app. UBS now values the non-financial ecosystem at close to $8 billion - exactly the current market cap of Tinkoff. Sber’s market cap is ~$80 billion.

Sberbank presented a subscription package and an array of hardware devices that would connect the home, TV, entertainment, and financial services. It has presented not one, but three (!) voice assistants with different personalities.

Additionally, ubiquity of Sberbank (leader of both retail and business banking) provides an opportunity to build a close loop integration between consumers and merchants. Sberbank has vision, money and scale to become THE ecosystem of Russia. With that it is a competitor not only to Tinkoff, but to any other consumer tech company in Russia, such as Yandex which is also building an ecosystem of its own.

So last September Yandex and Tinkoff announced merger plans, exciting the market about a formidable competitor to a growing Sberbank. But shortly after, the deal fell through. A disagreement about control, price, and future killed the deal. Both companies are now back to drawing tables, but it might not be the end of it.

Tinkoff Super App

With a strong competition not only from Sber and Yandex, but many other banks and consumer tech companies, Tinkoff has embarked on a Super App path, launching it in late 2019.

Sber, Yandex and many others are building similar consumer platforms. Moreover, the suite of non-financial services is practically identical (travel, ride hailing, food delivery, streaming, etc). But Sberbank has a massive customer base and unlimited budget, and Yandex has developed these services natively. So what is different about Tinkoff?

What about network effects?

Tinkoff benefited from extensive viral growth in early days, when word of mouth would spread about the innovative bank. Later, Tinkoff’s customer acquisition strategies were focused on partnerships and co-brands with popular internet services like Groupon. These strategies were adding tens of thousands of customers who came for a great product, but this wasn’t a network and customers didn’t need to be connected to benefit from the experience . For example, CashApp’s product was becoming better overall as more people were joining, and so customers were self-interested to bring their networks in. Kaspi, the other example, scaled retail and SME customers via free payments and then created a marketplace to tie them in even closer.

Tinkoff’s product is an insulated customer experience right now - taking a loan or putting in deposit doesn’t expand the network. They didn’t grasp the payments opportunity, and in any case, Sber’s sheer coverage has already solved that problem. They didn’t build e-comm marketplace, or community of customers (although Investments might pull it off).

So aside from a great banking product, there is no other customer pull. As a result, once the hype rolled over, Tinkoff’s acquisition costs started growing - on average Tinkoff spent $50 million per quarter last year (crudely translating to $90-$100 per new customer).

Building a competing Super App on top of a banking product (even though it is fast growing and customers like it), is going to be incredibly hard.

What about engagement?

Tinkoff Super App ticks some of the boxes, e.g. it directly owns customers, has access to their wallets, offers a broad suite of financial and non-financial products, and has near-zero marginal cost of serving users.

But because it doesn’t have strong network effects, its position is weaker. Tinkoff has a promising subset though - Tinkoff Investments and its community of retail investors, but that would grow independently from the Super App.

As a result, Tinkoff doesn’t benefit from key features of Super Apps like frequent touch points and low acquisition costs. Engagement measured as a share of Daily active users is relatively low for Tinkoff.

Moreover, it hasn’t been growing even after the launch of the Super App. It is ranked as no.20 in App Store and no.37 in Google Play in Russia.

Current upside from the Super App is increased interchange and commission income from lifestyle partners, but a year since launch details about the app are not forthcoming. Crucially engagement and stickiness hasn’t grown, despite top line customer additions. Yes, 40% of its revenue comes from non-lending, but it is nevertheless from other financial products like brokerage and insurance. So Tinkoff essentially remains a tech enabled bank, but bank nevertheless. And it is also how the market values it.

Tinkoff is a profitable and growing bank, with light cost structure and high dividends. It is clearly delivering customer and shareholder value, has a chance at becoming no.2 and maybe buy a few companies (e.g. Vivid Money is a neo-bank in Germany seeded and started by Tinkoff veterans). It should focus on what it does best.

What’s next?

Tinkoff Bank has been Oleg Tinkov’s largest and longest project and as a serial entrepreneur he is getting restless. Last month super voting shares held by Tinkov family trust were converted to ordinary voting shares. He wants to sell.

There is still a large opportunity ahead of Tinkoff Bank on its own (remember RoE of 50%!) - its customers are young, and there is plenty to be disrupted if not with Sber, then with others like VTB, Alfa-bank. Its prudent focus on performance and risk management makes it incredibly resilient - it has emerged stronger after every financial crisis, of which it went through two and a bit (07/08 global crisis, Russia’s sanctions re Crimea annexation, and ongoing pandemic). It stayed profitable throughout (bar one quarter).

No matter what’s next for Tinkoff Bank, it has achieved something incredible. There is a lot western neo-banks can learn from Tinkoff, e.g.:

lending can be done very profitably,

choosing profit ahead of scale is a guarantee of sustainability

For example, Revolut which has an equivalent number of customers has years ahead of reaching a comparable profitability.

If Tinkoff started in the UK, I believe it would have demolished the incumbents. A lot of people say that Tinkoff is undervalued because of Russia’s risks. I think the bigger story is that Russian banking service is so well developed that an incredibly rich banking product like Tinkoff had to fight with blood, sweat and tears to win some share. It is also a compliment to Sber, a bank with 280k staff and 96 million customers turning around like that - can’t imagine Lloyds, Barclays, JP Morgan really contemplating becoming a tech company right now.

I can’t pass by without telling you the funniest anecdote from the book. Tinkov writes that in 2016 they thought about acquiring hip western neo-banks and he met with Tom Blomfield of Monzo. When he was putting together a follow up meeting, Tom said he is going away for a two week holiday to India with his girlfriend. Tinkov writes that his jaw dropped: “Startup founder can’t go on a holiday, and moreover, tell about it to a potential partner. It is a losing story”, he writes. Monzo was not for sale, but I couldn’t describe the culture differences better than that. If you do business with a Russian partner, don’t tell them about your holiday plans.

As an extension Russia’s and for that matter Kazakhstan’s retail banking experience was miles ahead of HSBC/Barclays when I moved to the UK the first time in 2010s. For example, in the mid-2000s my bank in Kazakhstan had a complex online banking, instant spend notifications, spend analytics, partner resources, etc. All these features needed a fintech revolution to become a reality in the UK.

Excellent read!